May 2020 - More Black Swans and Credit’s Reckoning

Unless you were living under a rock, oil prices reached a record never thought possible. Aside for the sheer phenomena of a security trading for a negative value, its existence further highlights the circumstances that we find ourselves: extreme, Black Swan events are going to continue for the foreseeable future. Hopefully some of these will be positive, but more likely, major disruptions will be the trend in the financial markets for months to come.

The U.S. and major international economies function on massive credit markets. Credit has become ubiquitous with everyday life; we’re seeing that change right before our eyes. COVID-19 is becoming the biggest test to the credit markets and will change the way credit is used from hereon.

Source: Yahoo Finance

In early 2019, Euler Hermes and Allianz produced and article highlighting the re-leveraging of corporations, despite the longest expansion in U.S. history. They expanded this trend to a likely suggestion, “What if US Corporate Debt was Underestimated”. They argued that US corporate debt (as measured as a multiple of EBITDA) ran higher than calculated by the Federal Reserve, which at the time might not have been too precarious. But in an environment today, every extra amount of expansive credit, had leverage been measured more accurately, will have an exponential effect on the fallout today.

Today, the fluctuations in the leveraged loan market are quite simply profound pointing to some of these concerns. Below are two charts from S&P Global LCD. The two charts displays the growing number of leveraged loans downgraded by S&P Global Ratings and the growing percentage of outstanding loans now deep in junk status (below BB-). Leveraged loans are unsurprisingly one of the first areas of the credit market to show signs of stress. If leveraged loans is to have a major fallout, it will affect the ability of more cyclical or riskier businesses from obtaining credit in the years ahead.

On the consumer side, major consumer credit providers have taken a beating and remain at depressed levels, despite an 11% rebound in the S&P 500 as of April 22nd (which this author would argue is a bit Pollyanna). As the chart shows, the SPDR Financial Sector ETF (Ticker: XLF) is down 31.5% YTD. It This ETF includes some of largest financial institutions in the U.S., who will likely fare better in this cycle than consumer credit focused businesses. Other more consumer credit-centric businesses have not fared as well. The other companies listed are ALLY: Ally Financial, SYF: Synchrony Financial, TREE: Lending Tree, and LC: Lending Club.

For some context on the headwinds these businesses are facing, Ally Financial reported that 25% of customers have asked for some form of payment deferral. The credit arms for GM and Ford are bracing for the loss of billions as used car prices plunge.

Easy access to credit has become a pillar of American society. We’ve become exceptionally creative in using new technologies to provide ever-more credit options for nearly anything (think peer-to-peer lending). The dearth of credit options and our views on consumer credit will be forced to change as a result of this.

Source: Yahoo Finance

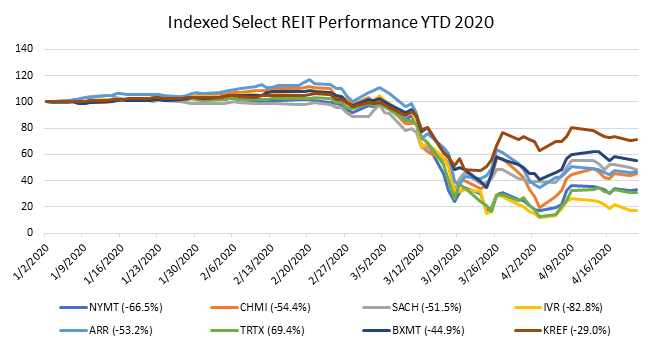

Finally, another credit market to watch is real estate. The final chart displays the indexed performance of select major REITs (includes both consumer and commercial mortgages) in the U.S. The hardest hit of the select group is IVR: Invesco Mortgage Capital, down over 80% year-to-date. As the effects of Coronavirus shutdown reverberate throughout the economy major uses of credit (albeit good uses of credit) will be forced to contend with the claims and attention of all the credit extensions the American consumer has put-on themselves.

Source: Yahoo Finance

Credit has been the answer for many aspects of American consumerism:

• Go to college -> take out student loans

• Buy a car -> take out a car loan

• Buy a house -> take out a mortgage

• Pay for a major expense -> take out a personal loan

• Everything else -> use a credit card!

The little-engine that could (U.S. consumption) has become completely dependent on credit, it now threatens our recovery and the functioning of our economy.

By and large, credit is a beneficial to the economy. It provides economic mobility for millions, and capital for businesses to grow, but unfortunately our hyper-consumption lifestyle has pushed it too far. We’re Americans, we’re perpetually optimistic, Europeans look at us with bemusement, the world looks at our economy with envy and aspiration. In order for our economy to make it through this challenge and thrive in the decades ahead our relationship with credit needs to be examined. As the Roman Philosopher Seneca the Younger best put it: