March 2020 - Market Research and Commentary

Not just the Stock Market – Credit Markets feel the pain

Market conditions have changed at a feverish pace, never before has the stock market so quickly entered a bear market. Unlike 2018, the most recent comparison, monetary policy has much less ammunition to buoy this market.

This month’s newsletter will take a look at the rapidly changing conditions in the credit markets and potential moves to come. Major industries such as Real Estate and Oil and Gas have billions of bonds floating just above investment grade status. As these economic conditions prolong, downgrades become inevitable forcing selling down the road. In extreme situations the volatility buffer credit can provide quickly becomes replaced with binary outcomes (stable investments or defaults). Expect to see continued volatility in the credit markets particularly for highly levered industries and businesses.

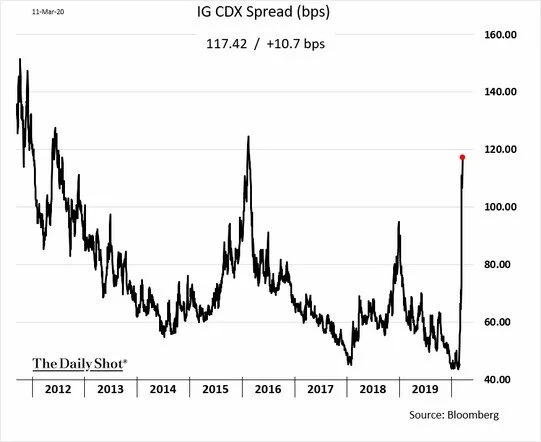

Chart 1: Investment Grade Credit-Default Swaps have Skyrocketed

Other significant movements in credit spreads include High Yield Credit Default Swap spreads expanding 600 bps, and High-yield Energy Credit Default Swaps expanding almost 1,600 bps (Daily Shot)

Leveraged loans have started to take a beating, falling in line with low-graded bonds. More specifically two leveraged oil ETP’s are closing following a rout in the oil & gas market.

Chart 2: High Yield and Leveraged Loan Indexes

Chart 3: Oil and Gas ETP Closes

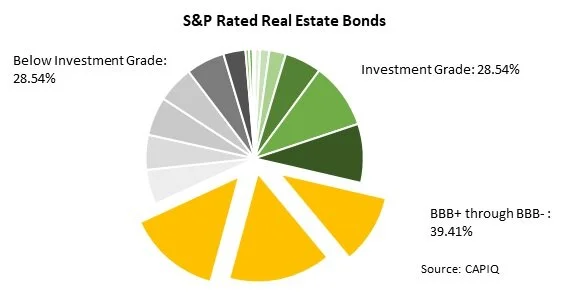

Turning to specific segments of corporate credit, below are three pie charts summarizing bond ratings for Real Estate Bonds (U.S., Europe and Asia-Pacific), Financial Services (U.S., Europe and Asia-Pacific), and Oil and Gas (U.S. and International). Portions of the pie charts in green are investment grade bonds, yellow are BBB bonds (e.g. potential for downgrading) and below investment grade. As it stands financial services appear well capitalized but large portions of real estate and oil and gas bonds could be pushed to below-investment grade. Given the “investment-grade” requirement for major institutional investors such changes could produce a broader sell-off.

Chart 4: S&P Bond Ratings for Real Estate

Chart 5: S&P Bond Ratings for Financial Services

Chart 6: S&P Bond Ratings for Oil & Gas

Finally, as we look ahead to the Fed and Treasuries response it’s worth noting the current state of Fed Balance Sheet, market liquidity and how much ammunition the Fed has to stimulate the economy. Not to be a harbinger of pessimism, but given the extensive and unprecedented level of monetary stimulus in the last 10 years one has to seriously question how well comparable levels of stimulus can work in the future.

Fed Funds Rate: The Fed Funds rate has never been lower heading into what appears to certainly be a recession. Following the 500 bps cut the week of March 2nd, the Fed has only 1000 bps before it hits a 0% effective Fed Funds Rate, not exactly a lot of ammunition to support a protracted downturn.

Chart 7: Fed Funds Rate

Fed Balance Sheet: Following the short quantitative tightening in 2019 the Fed made little progress in reducing its balance sheet. After repo market rates spiked in the fall of 2019 it quickly went back into expansion mode.

Chart 8: Fed Total Assets

Market Liquidity: The reason for questioning and criticism is partly stemmed by the level of liquidity in the market. Using money market funds as a proxy, trillions of dollars are still sitting on the sidelines, the question is will more liquidity prompt investors to change their behavior attitudes to the current economic conditions and buy in?

Chart 9: Money Market Funds - Asset Levels