August 2019 - Market Research and Commentary

In the last five years, an intriguing trend has emerged in fixed income markets around the world. Across all classes of fixed income securities, from municipal bonds to corporate bonds, markets have seen an immense inflow of cash into bonds and various fixed income funds. With investors pouring money into fixed income and bond funds, there has also been a notable concentration of buyers, especially in the municipal bond market.

Throughout the first half of 2019, capital flowed into bonds and bond funds at a record pace as investors retain a cautious sentiment about global markets. As of the end of July, there have been 28 consecutive weeks of inflows into bond funds, in the aggregate; this has brought the total inflows on the year to a record $254 billion, with projections of $455 billion on an annualized basis for 2019. The magnitude of these inflows is particularly noticeable when compared to the $1.7 trillion in bond fund inflows in the 11-year period of 2008-2018.

Chart I - 2019 YTD Cumulative Global Bond Fund Inflow

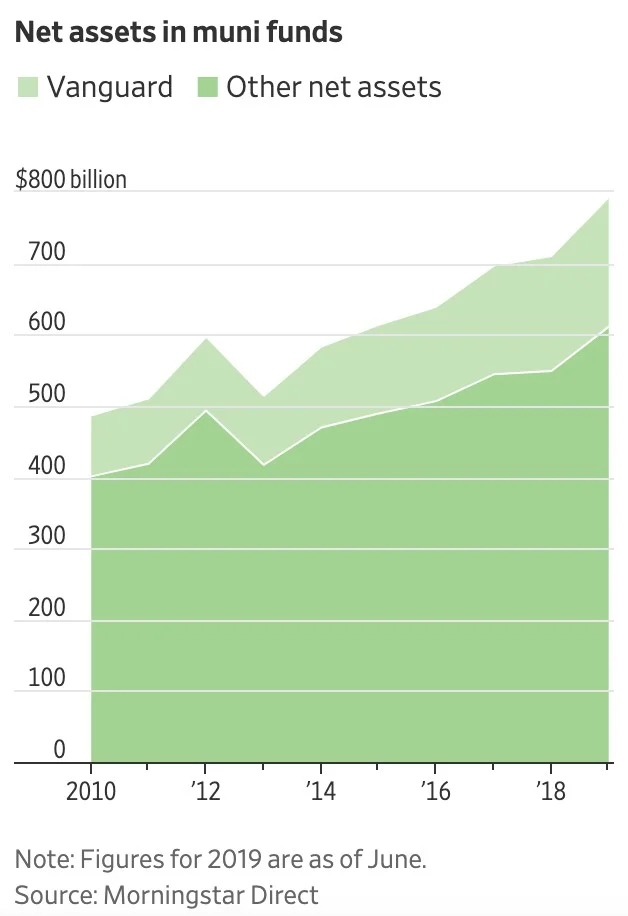

With this profound inflow into bond funds, another trend has emerged. The cash inflows into bond funds are concentrated amongst a handful of some of the world’s largest institutional investors; this is particularly evident in the municipal bond market. Within this $4 trillion market, professional money managers and mutual funds have begun to invest heavily in both high-grade and low-grade municipal debt. This concentration of cash inflows has increased rapidly since 2009, according to data from the U.S. Federal Reserve Bank. The 50% increase in institutional holdings of municipal fixed income that has occurred since 2009 means that institutional holdings of local, state and federal government debt is currently sitting at $738.6 billion. The establishment of municipal bond funds has benefited large institutional money managers like Nuveen and Vanguard. These funds also allow individual investors the opportunity to diversify fixed income investments and helps explain some of the increased demand or aggregate inflows.

Chart II - Net Assets to Municipal Bond Funds

This concentration and volume of inflows in both the municipal bond market and the broader fixed income markets are expected to continue as the global economic forecast remains uncertain. In the year-to-date period, mutual funds and ETFs that track the U.S. equity markets have seen cash outflows of $45.4 billion. While outflows from equity funds have decreased in the month of July as a result of impending rate cuts by the Federal Reserve, it is projected that investors will continue the broader trend of moving their investments from equity positions into fixed income mutual funds as the global economy becomes more uncertain. If investors are to continue this trend, this could lead to an even greater concentration of bonds held by a few of the largest asset managers under the argument that investors like to follow the crowd meaning the most popular funds only get more popular.

Chart III - Aggregated Bond and Equity Funds Inflow

These inflows into bond funds could be a strong indicator of what’s to come for the global economy in the next 12 months. As both personal and institutional investors flow into fixed income funds over their equity counterparts, there is an implicit sentiment that global equities are running out of steam due to weak future growth. This continued flight to the relative safety of bond funds comes at a particularly interesting time as equities continue to surge through the loses at 2018 year-end. With the first interest rate cut anticipated since the recession we are in an interesting time of fairly positive economic news but positioning by the Fed that is anticipating worsening conditions.

As the final chart shows, the probability of a recession has never been higher since the last recession, but as the chart shows these factors are no-where near a perfect predictor. The flight to fixed-income could be a last grasp by investors to capture higher yields before a downward parallel shift in the yield curve occurs. Nonetheless, with another month of trade uncertainty continuing, no clarity on Brexit and decreased fiscal stimulus in the U.S., we all might enjoy the increased certainty provided by fixed income.

Chart IV - Multi-factor probability of recession